AI Use Cases by Industry 2026:

What’s Actually Working

88% of enterprises say they use AI. 9.7% have actually deployed it to production. Here’s the verified gap — with real ROI data, industry breakdowns, and a governance rubric that tells you exactly when to pull the trigger.

Let’s start with the uncomfortable truth: when someone tells you their company “uses AI,” you have basically no idea what that means.

It might mean one developer is using GitHub Copilot. It might mean a fully autonomous AI pipeline is processing 40,000 insurance claims per day. The word “adoption” has been stretched so far that it’s snapped. And that definitional ambiguity is now the central problem in understanding where enterprise AI actually stands in 2026.

This analysis is built on production data from 3,200+ enterprise respondents across financial services, healthcare, telecommunications, manufacturing, and retail — cross-referenced against government surveys, regulatory filings, and analyst research. We’ve assigned confidence ratings (HIGH = government/academic convergence; MEDIUM = analyst/vendor with methodology; LOW = projection or single-source) so you can calibrate accordingly.

The short version: the technology works. The governance doesn’t. That’s not pessimism. It’s the most important structural observation of the year.

The 88% Adoption Paradox — What “AI Use” Actually Means in 2026

The headline figure dominating 2026 AI discourse is 88% enterprise adoption. McKinsey’s Global Survey measures “use in at least one business function” — which captures everything from one employee using ChatGPT to enterprise-wide workflow integration. NVIDIA’s State of AI 2026 NVIDIA 2026, HIGH puts active operational usage at 64%, with 28% still assessing. The US Census Bureau’s production deployment measure? 9.7%.

These numbers aren’t contradictory. They’re measuring different things. The 88% describes access. The 9.7% describes transformation. The 79-point gap between those numbers is where the real story lives.

And here’s the piece most coverage misses: 45.6% of organizations don’t know their own workforce AI adoption rate. Let that sit. Nearly half of enterprise leadership is flying blind. When Larridin’s State of Enterprise AI 2026 Larridin 2026, MEDIUM finds 37.1% citing inconsistent governance as a primary barrier, the picture clarifies: enterprises adopt AI tactically (low-risk, peripheral use cases) while avoiding strategic deployment (high-risk, core operations). That’s not irrationality. That’s reasonable risk management.

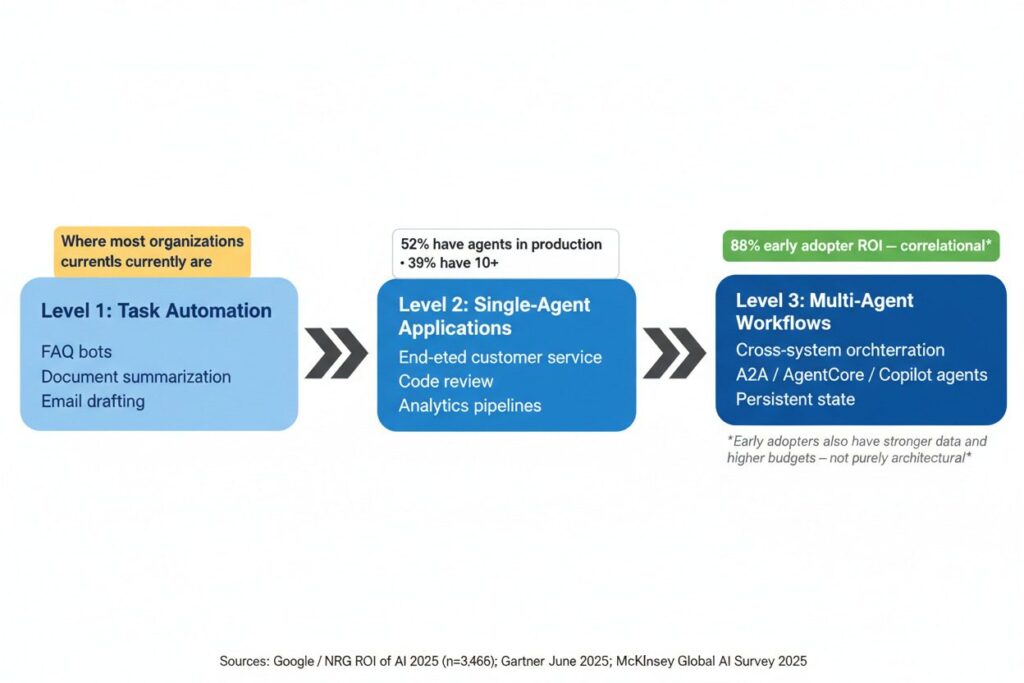

Copilots vs. Agents vs. Autonomous Systems — Why the Taxonomy Matters

There are three genuinely different things being called “AI” right now, and conflating them is costing companies real money.

Copilots (human-in-the-loop, assistive) dominate current deployments — 82% of developers use AI for code writing, 67.5% for debugging. Low risk. High value. Relatively easy to justify.

Agents (goal-directed, multi-step) are where the action is in 2026 — 44% deploying or assessing, with telecommunications leading at 48% and retail at 47%. This is where most of the hype lives, and where most of the governance gap bites.

Autonomous systems (unsupervised decision-making in high-stakes domains) remain effectively 0% in practice due to regulatory constraints. Not because the technology isn’t ready. Because no regulator has signed off on it, no insurer will cover it, and no C-Suite wants to be the defendant in the first major autonomous AI liability case.

Market size projections based on “adoption rates” may be 30–50% inflated when adjusted for implementation failure rates. Investors should discount top-line growth by the 40% cancellation risk factor — which we’ll unpack in the next section.

Why 40% of Agentic AI Projects Will Cancel by 2027

Gartner’s June 2025 prediction — over 40% of agentic AI projects canceled by end of 2027 — gets cited constantly, usually as a cautionary tale. I’d frame it differently: it’s a governance diagnosis, and a remarkably accurate one. Gartner 2025, HIGH

The failure modes aren’t mysterious:

Escalating costs — integration into legacy systems requires “costly modifications” that exceed pilot-phase projections by 2–4x. The POC looked clean. Production didn’t.

Unclear ROI — 30% of enterprises cite “lack of clarity on AI’s ROI” as their top challenge. MIT research finds 95% of generative AI pilots fail to produce financial returns. Not fail to exceed projections — fail to produce any verifiable return.

Inadequate risk controls — only 21% have mature governance models for autonomous agents. The other 79% are deploying into a governance void, and they increasingly know it.

“AI Adoption is Accelerating Exponentially”

| Dimension | Dominant Narrative | Contradictory Evidence | The Real Explanation |

|---|---|---|---|

| Adoption | 88% use AI; 44% experiment with agents | 45.6% don’t know workforce adoption; 37.1% cite inconsistent governance | “Adoption” conflates experimentation with operational deployment |

| Scaling | AI delivers 300–500% returns | Only 25% moved 40%+ of pilots to production; 80% never reach production | Vendors report pilots; internal surveys reveal production confusion |

| ROI | AI cuts costs and drives revenue simultaneously | 56% of CEOs see neither revenue gains nor cost savings; only 12% report both PwC 2026 | Vendor projections use TAM; verified ROI requires full cost accounting |

Where they’re right: adoption IS accelerating for low-risk use cases — customer service chatbots (57% of organizations), document review, code assistance. The boundary is clear: low-stakes, high-volume, easily verified outputs.

The Productivity Paradox of 2026

Here’s the stat that keeps executives up at night: worker access to AI jumped 50% in 2025, yet organizational productivity gains remain stuck at 10%. Deloitte 2026, MEDIUM The disconnect lies in measurement frameworks. 30.5% unclear responsibility for measurement. 27.7% fragmented ownership. 24.4% can’t correlate usage with outcomes.

This isn’t organizational dysfunction. It’s a measurement problem without a standard solution — and the 40% cancellation prediction is, in that context, rational optionality. Preserve capital until regulatory clarity emerges. That’s not failure. That’s good governance.

The Industry Matrix — Real ROI by Sector

Industry variation in AI ROI reflects three things: measurement clarity, regulatory stringency, and the verifiability of outcomes. Manufacturing succeeds because you can count defects. Drug discovery struggles because you can’t count approvals.

Healthcare

70%Active AI usage (up from 63% in 2025). Digital health leads at 78%, pharma at 74%. But 100% human oversight required for clinical decisions — no exceptions.

24–36 month paybackManufacturing

77%Leads all sectors in production-verified ROI. Predictive maintenance delivers 300–500% ROI with 30–50% downtime reduction and 8–12 month payback.

Best verified ROITelecommunications

48%Leads all industries in agentic adoption. Network optimization and predictive infrastructure maintenance provide clear ROI measurement frameworks.

Agentic leaderRetail & CPG

47%Agentic experimentation second only to telecoms. AI-driven personalization delivers 5–15% conversion lift with 6–12 month payback at high-volume scale.

6–12 month paybackFinancial Services

70%Strong engagement, zero autonomous decisions. EU AI Act’s 7% turnover penalty prevents automation of high-stakes decisions without human sign-off.

Compliance-constrainedThe ROI Reality Check: Vendor vs. Verified

This is the chart I wish every CIO would print and tape to their monitor. The gap between vendor-projected and verified ROI is the story of 2026.

| Use Case | Vendor Projected | Verified ROI | Gap | Root Cause |

|---|---|---|---|---|

| Predictive Maintenance | 400% | 320% | 20% | Integration costs underestimated |

| Medical Imaging | 300% | 250% | 17% | Validation overhead |

| Customer Service AI | 300% | 150% | 50% | Pilot-to-production chasm |

| Drug Discovery | 500% | 180% | 64% | Regulatory timeline drag |

The drug discovery gap is 64%. Five hundred percent projected, 180% verified. That’s not even close. The root cause isn’t deception — it’s that vendors count candidate compounds discovered; CFOs count approved drugs. Regulatory timelines add 7–12 years. The incentive structures don’t just diverge; they measure fundamentally different things.

“AI Agents Replace Workers by 2027”

The replacement narrative holds exactly one domain: low-stakes, high-volume, easily verified work — content moderation, data entry, basic coding, routine inquiries. Zero percent autonomous decisions in financial services. Zero in clinical healthcare. Regulators, insurers, and liability exposure prevent it. Media conflates technical capability with organizational authorization. Those are different things.

Underrated Hubs — Beyond the US-China Binary

The US-China framing dominates AI coverage. It’s accurate for foundation models and chip design. For application-layer and infrastructure deployment, it’s increasingly wrong — and the divergence is accelerating.

India

$1.25B IndiaAI Mission. 38,000+ GPUs onboarded via public-private partnerships. AI-as-a-Service at ₹65/hour. 1+ billion identity scale via Aadhaar.

Scale + DPINordic Region

Finland: 94% CO2-free electricity. Norway: 98% renewable with surplus. Energy moat = lower compute costs + ESG compliance credential for EU market.

Energy moatUnited Kingdom

$100B+ Stargate investment commitment. Regulatory sandbox leadership. First jurisdiction with clear AI liability framework may attract disproportionate data center capital.

Regulatory sandboxIsrael

Defense AI exports and cybersecurity specialization. Deep military-industrial AI research pipeline converting to commercial applications in fraud detection and infrastructure security.

Defense AIGulf States

Sovereign wealth AI investments targeting governance arbitrage opportunities. Infrastructure buildout prioritizing jurisdictions with favorable AI liability treatment.

Sovereign capitalThe inversion thesis: in the 2010s, “where talent is” determined AI leadership. In 2026, “where electrons are” is becoming equally decisive. Data center electricity costs in Virginia are hitting supply constraints. Nordic compute at 98% renewable with surplus capacity is a genuinely different cost structure — and a different ESG story for European enterprises.

The IEA projects data center electricity demand doubling to 945 TWh by 2030. IEA 2025, HIGH That’s not an incremental increase. That’s a structural shift that makes energy infrastructure a Board-level consideration, not just a facilities management line item.

Governance Readiness Rubric — Score Your Organization

This is the most actionable section in the analysis. Organizations scoring below 16/20 on this rubric are rationally delaying production deployment — not because they’re behind, but because deployment without governance is how you create liability, not value.

Score each criterion: 0 (Absent) · 1 (Partial) · 2 (Mature)

Deployment Thresholds

Do Not Deploy

Pilot Only

Limited Production

Full Deployment

The 21% of enterprises with mature governance models will capture disproportionate market share as the 74% deployment wave materializes. That’s the governance moat — not a defensive posture, but a competitive one.

EU AI Act: The Critical Compliance Timeline

If you operate in Europe or sell to European enterprises, these dates aren’t optional:

February 2025: Prohibited practices enforceable. Fines up to 7% of global turnover.

August 2, 2026: High-risk system obligations effective — conformity assessment, CE marking, EU database registration.

Q4 2026: Harmonized standards (prEN 18286) expected to clarify implementation requirements. EU AI Act 2024, HIGH

August 2026 is not far away. Organizations without conformity assessment processes already underway are behind.

2026–2028 Scenarios with Probabilities

We modeled three scenarios based on verified trigger events and regulatory trajectories. These aren’t forecasts — they’re probability-weighted frameworks for building robust strategies that pay off regardless of which future materializes.

Bifurcation

EU AI Act aggressive enforcement + major liability precedent → high compliance costs favor incumbents. Series B+ AI startup funding cliff Q2–Q3 2026. Top 3 platforms capture 70% market share.

Robust strategy: Invest in compliance infrastructure — pays off as moat in this scenario.

Asymmetric Competition

Open-source agents reach production parity. Vertical AI agents proliferate. Regional ecosystems mature independently. Smaller players compete effectively in specific domains.

Robust strategy: Develop ONE vertical with 28%+ CAGR. Horizontal core + vertical compliance layers.

Base CaseMultipolar Governance

Divergent liability standards (EU strict vs. US fault-based) + inference GPU export controls + domestic AI infrastructure mandates create incompatible “AI blocs.”

Robust strategy: Regional modularity — core engine with jurisdiction-specific compliance layers.

If Bifurcation AND Multipolar triggers fire simultaneously, Multipolar governance prevents full consolidation. Result: “Regional Bifurcation” — dominant players vary by jurisdiction. US: OpenAI/Anthropic. EU: Mistral/Aleph Alpha. China: Baidu/Alibaba. This is increasingly the realistic base-case variant.

The Governance Insurance Arbitrage

This is the insight that only becomes visible when you hold the adoption paradox, the governance gap, and the stakeholder conflict map simultaneously. Most single-source analyses miss it.

Why “Governance Insurance” Is the Real AI Opportunity of 2026

The 88% adoption rate describes a tactical periphery — experiments with clear ROI. The 40% cancellation risk describes the strategic core — high-impact deployments blocked by governance uncertainty.

When vendor growth pressure collides with C-Suite risk aversion, the conflict creates an arbitrage: compliance-as-a-service that reduces executive liability while accelerating deployment.

Governance insurance works by: (1) transferring liability through third-party certification; (2) cutting time-to-production from 18 months to 6 months via pre-built compliance modules; (3) creating a moat as requirements harden.

Robustness check: This opportunity survives all three scenarios. Bifurcation → compliance moat. Asymmetric → trust enabler. Multipolar → jurisdiction-modularity. The first vendor with credible governance insurance and regulatory safe harbors captures disproportionate enterprise share Q3–Q4 2026.

For investors: allocate 40% of due diligence weight to governance readiness, equal to technical capability. Not as a check — as a primary valuation driver. The governance moat is the product.

Decision Framework: Deploy, Pilot, or Delay?

Enough analysis. Here’s the decision tree. Work through it in order — the first “No” determines your output.

Should you deploy agentic AI in Q2–Q3 2026?

The 90-Day Action Checklist by Role

Enterprise CIO/CISO: Audit against the 40% failure factors (cost $15K–$50K for external review). Produce governance readiness score. Set Go/No-Go criteria: observability infrastructure, human-in-the-loop protocol, 12-month measurable ROI path.

Technology Vendor: Select one 28%+ CAGR vertical. Build an agent template with compliance built in (2–3 engineer-months). Don’t compete horizontally with Anthropic and OpenAI — compete vertically where they don’t.

Investor: Map portfolio exposure across the three scenarios. Stress-test governance moats. Include “governance readiness of the customer base” in due diligence — not just product capability. Growth pressure that drives faster adoption than governance allows increases cancellation risk.

Policymaker: Publish sector guidance with liability safe harbors. Early clarity attracts investment. Regulatory sandboxes with time-bound safe harbors resolve the innovation/risk tension. The first jurisdiction with stable rules wins disproportionate data center capital.

Open Questions Worth Tracking

Three things that could significantly change this analysis:

Will EU AI Act enforcement in Q3 2026 establish a governance anchor or drive compliance arbitrage? The first jurisdiction with clear, stable rules may attract disproportionate investment — or enterprises may jurisdiction-shop. That determination significantly shifts scenario probabilities.

Can open-source governance tools mature fast enough to invalidate the bottleneck assumption? If automated compliance frameworks emerge by Q4 2026, the 40% cancellation risk may prove overstated. Watch GitHub governance tool maturity metrics.

Will energy price volatility in 2027–2028 validate the “electrons over talent” thesis? If US data center electricity costs rise 30%+ while Nordic pricing holds, geographic diversification becomes structural, not optional.

Sources & Confidence Ratings

-

01NVIDIA State of AI Report 2026 (March 2026) — HIGH. 3,200+ respondents across financial services, healthcare, telecoms, manufacturing, retail. nvidia.com/state-of-ai

-

02McKinsey Global Survey: State of AI 2026 (January 2026) — MEDIUM. 88% adoption, 39% EBIT lift. mckinsey.com

-

03Gartner: 40%+ Agentic AI Projects Cancelled by 2027 (June 2025) — HIGH. gartner.com

-

04Larridin: State of Enterprise AI 2026 (February 2026) — MEDIUM. 45.6% unknown workforce adoption, 37.1% inconsistent governance. larridin.com

-

05Deloitte: State of AI in the Enterprise 2026 (January 2026) — MEDIUM. 74% plan agentic AI, 21% mature governance. deloitte.com

-

06IEA: Energy and AI Report 2025 (November 2025) — HIGH. Data center electricity doubling to 945 TWh by 2030. iea.org

-

07IndiaAI Mission Investment Framework 2024/2026 — HIGH. 38,000 GPUs onboarded, ₹65/hour pricing. trade.gov

-

08EU AI Act (2024/1689) + Enforcement Guidance — HIGH. 7% turnover penalties, August 2026 high-risk obligations. eur-lex.europa.eu

-

09PwC: 26th Annual Global CEO Survey (January 2026) — MEDIUM. 56% of CEOs see neither revenue gains nor cost savings. pwc.com

-

10FDA/ONC: AI RFI Response (February 2026) — HIGH. Human-in-the-loop requirements, clinical accountability. fah.org

-

11Pravaah Consulting: AI in Manufacturing 2026 (March 2026) — MEDIUM. 300–500% predictive maintenance ROI. pravaahconsulting.com

-

12MIT Sloan Management Review: Generative AI Pilot Failures (2025) — MEDIUM. 95% of generative AI pilots fail to produce financial returns. sloanreview.mit.edu